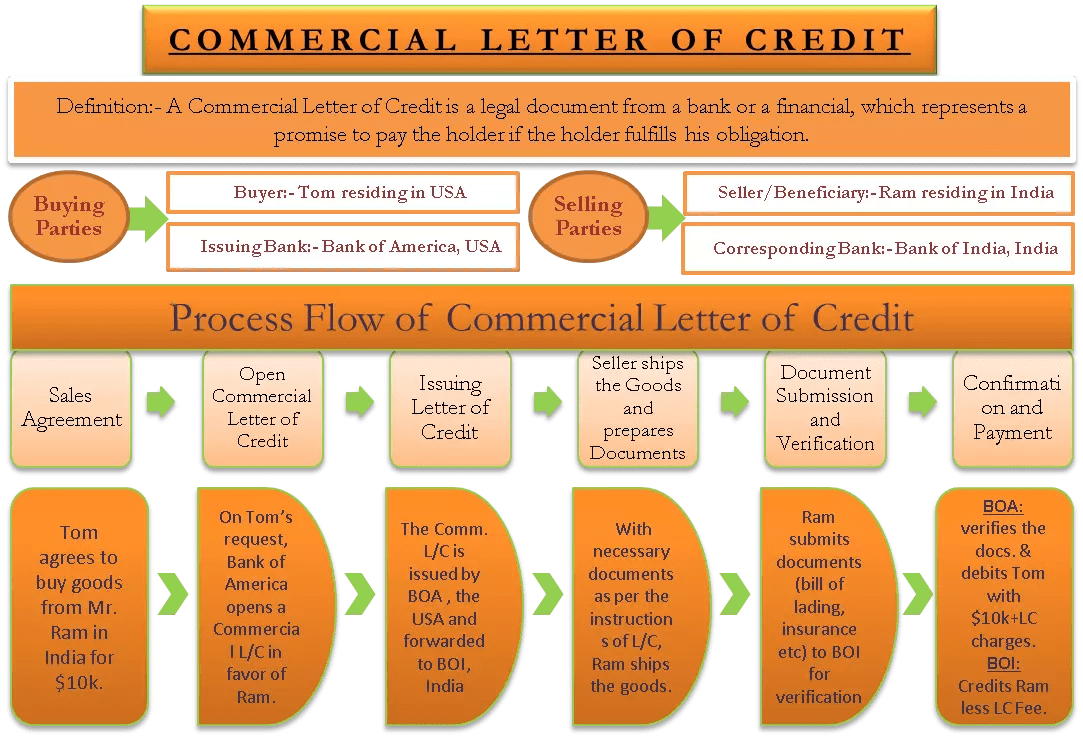

Let us understand the process flow of letter of credit with an example. There are four parties involved in a commercial letter of credit as follows:

- Buyer – Tom residing in the USA

- Issuing Bank – Bank of America, the USA

- Correspondent Bank – Bank of India, India

- Beneficiary/Seller – Ram residing in India

STEP 1: SALES AGREEMENT

On 1st January 2018, Mr. Tom from the USA agrees to buy goods worth USD 10,000.00 from Mr. Ram in India. During the negotiations, it was agreed that payment would be done in a commercial letter of credit.

STEP 2: OPENING INSTRUCTIONS

Mr. Tom requests Bank of America to open a letter of credit of USD 10,000.00 in favor of Mr. Ram. The Bank of America checks Mr. Tom’s creditworthiness and completes the required formality to issue a letter of credit for this transaction.

STEP 3: ISSUING LETTER OF CREDIT

On 8th January 2018, The Bank of America issues the requested letter of credit that expires 90 days from the date of issue and forwards it to the corresponding bank i.e. Bank of India. The corresponding bank is usually located in the country in which the seller resides, in our example, it is in India. Bank of India will authenticate the letter of credit and send it to Mr. Ram. It is necessary that Mr. Ram exports the goods and submits the required documents before the expiry of the letter of credit. If not then the bank of America is not obliged to pay if Mr. Tom doesn’t.

STEP 4: SELLER SHIPS THE GOODS AND PREPARES DOCUMENTS

On 1st March 2018, Mr. Ram ships the goods to Mr. Tom and prepared the required shipping documents as per the instructions of the letter of credit. The usual documents required are – commercial invoice, packing list, transport document (bill of lading or airway bill) and insurance policy. Some banks require additional documents but these are necessary.

STEP 5: DOCUMENT SUBMISSION AND VERIFICATION

Mr. Ram submits the documents to the Bank of India. Bank of India checks all documents to confirm whether they are in compliance with the instructions of the letter of credit. Thereafter the Bank of India sends the documents to Bank of America and asks for payment.

STEP 6: CONFIRMATION AND PAYMENT

Bank of America again checks the documents for compliance and if all the documents are in place, it debits Mr. Tom’s account of USD 10,000.00 + letter of credit fees and pays USD 10,000.00 to Bank of India who further deducts its own fees and deposits the remaining amount in Mr. Rams account. As the banks are involved in the transaction, both parties are secured that the other one will fulfill its obligation the bank will intervene. There are many different types of letters of credit, but that is a story for another day.